![]()

IIA-CIA-Part2試験をパスするなら弊社のCertified Internal試験パッケージを今すぐゲットして合格せよ

完全版最新の2023年最新のIIA-CIA-Part2試験問題集テストガイド、専門トレーニングJPNTest

IIA-CIA-PART2試験は、内部監査の実践に焦点を当てた内部監査協会(IIA)が提供する認定試験です。この試験は、内部監査の計画、実行、コミュニケーション、リスク管理などの分野で候補者の知識とスキルをテストするように設計されています。この認定は、内部監査の実践における能力と専門知識のレベルを示すため、内部監査の専門職で非常に尊敬されています。

IIA-CIA-Part2 試験に合格するためには、候補者は内部監査または関連する経験を最低2年以上持っている必要があります。また、内部監査の基礎をカバーする IIA-CIA-Part1 試験を受験している必要があります。IIA-CIA-Part2 試験は、100問の多肢選択問題から構成され、2時間半以内に完了する必要があります。試験に合格すると、内部監査の実践における専門知識を証明する CIA 認定を取得することができます。この認定は、雇用主から高い評価を受け、内部監査の職業内でのキャリアアップの機会を提供することができます。

内部監査試験の練習としても知られるIIA-CIA-PART2試験は、内部監査機関(IIA)が提供する認定です。この試験では、現実世界の状況で内部監査の概念、技術、およびツールを適用する候補者の能力を評価します。この試験に合格することは、キャリアを進め、専門知識を実証しようとする内部監査人にとって重要なマイルストーンです。

質問 # 155

Which of the following best defines an engagement conclusion?

- A. An opinion that must be included in the engagement final communication.

- B. A recommendation for corrective action.

- C. An auditor's determination of the cause of an engagement observation.

- D. An auditor's professional judgment of the situation which was reviewed.

正解:D

解説:

Section: Volume B

質問 # 156

Which of the following is not true regarding the management of internal audit resources?

- A. Skills availability must be aligned with financial constraints.

- B. A minimum level of information technology knowledge is necessary.

- C. The adequacy of internal audit resources is ultimately a board responsibility.

- D. Resources include external service providers and computer-assisted audit techniques.

正解:A

質問 # 157

An internal auditor compared the number of human resources professionals per employee withindustry standards. This comparison would assist the auditor in evaluating which of the following areas?

- A. Adequacy of controls over hiring new employees.

- B. Degree of compliance with human resources policies.

- C. Current level of performance of the human resources department.

- D. Sufficiency of controls over payroll rate increases.

正解:C

質問 # 158

Which of the following activities would be performed during a benchmarking consulting engagement?

I.Collect data relevant to the benchmarking process.

II.

Review all business processes.

III.

Define critical success factors.

IV.

Identify performance gaps.

- A. II and IV only.

- B. I, II, and III only.

- C. I, III, and IV only.

- D. I and III only.

正解:C

質問 # 159

An internal auditor is planning an assurance engagement. The auditor first reviews the department's business objectives. What is the next step?

- A. Evaluate potential risks.

- B. Establish risk management roles.

- C. Review control activities.

- D. Set the scope of the engagement.

正解:A

解説:

Section: Volume C

質問 # 160

Which of the following documents should the chief audit executive review and approve?

1.Workpaper retention policy.

2.Audit committee meeting minutes.

3.Internal audit handbook.

4.Quarterly financial statements.

- A. 1, 3, and 4 only

- B. 1 and 2 only

- C. 2 and 4 only

- D. 1 and 3 only

正解:D

質問 # 161

The following is an excerpt from an audit engagement workpaper:

-A Company -Accounts Receivable -Date

Objective. To determine if the computer system is correctly recording all accounts receivable transactions.

Procedures: Judgmental selection of a sample of all accounts receivable balances greater than $50,000 for positive confirmation of balances.

Conclusion: Based on the results of testing wherein all but three confirmations were returned, the accounts receivable balance is fairly presented in all material respects.

Which of the following is true regarding the workpaper?

- A. The audit procedures used are not consistent with the audit objective.

- B. A conclusion should be reached only for the results of overall testing, not for individual procedures.

- C. It is not appropriate to judgmentally select a sample when testing accounts receivable.

- D. The format of the workpaper does not conform to the standard format for workpapers.

正解:A

質問 # 162

Which characteristic of risk assessment makes it a useful tool for audit planning?

- A. It evaluates the probability that an event or action may adversely affect the organization.

- B. It provides a list of auditable activities in the organization.

- C. It provides a process for identifying and analyzing potentially adverse effects.

- D. It ranks the severity of potentially adverse effects on the organization.

正解:C

解説:

Section: Volume C

質問 # 163

An internal auditor is reviewing a new automated human resources system. The system contains a table of pay rates which are matched to the employee job classifications. The best control to ensure that the table is updated correctly for only valid pay changes would be to:

- A. Require a supervisor in the department, who does not have the ability to change the table, to compare the changes to a signed management authorization.

- B. Require that all pay changes be signed by the employee to verify that the change goes to a bona fide employee.

- C. Limit access to the data table to management and line supervisors who have the authority to determine pay rates.

- D. Ensure that adequate edit and reasonableness checks are built into the automated system.

正解:A

質問 # 164

Which of the following files, when compared with billing records, would provide the best source of information for determining if all goods shipped are billed to customers?

- A. Customer purchase orders.

- B. Pre-numbered customer invoices.

- C. Accounts receivable transactions.

- D. Pre-numbered shipping documents.

正解:D

質問 # 165

Which of the following audit techniques provides for continuous monitoring and analysis of computer transactions for detailed auditing?

- A. Integrated test facility.

- B. Embedded audit routines.

- C. Test data.

- D. Parallel simulation.

正解:B

質問 # 166

Under what circumstances would internal audit not become involved when intentional misconduct is suspected?

- A. Management is involved in wrongdoing.

- B. Management is running a parallel investigation.

- C. Management does not maintain strong internal controls.

- D. Management does not believe a trusted employee could be guilty.

正解:B

質問 # 167

According to IIA guidance, which of the following are acceptable strategies for an internal audit activity (IAA) to establish or build relationships?

- A. Assist executives with their administrative and governance responsibilities, and encourage all IAA members to develop relationships with the organization's executives.

- B. Assist executives with their administrative and governance responsibilities, and ensure that all communications with the board are formal audit reports or preset agendas.

- C. During an engagement, restrict communications with affected executives to matters pertaining to the engagement; and encourage all IAA members to develop relationships with the organization's executives.

- D. During an engagement, restrict communications with affected executives to matters pertaining to the engagement; and ensure that all communications with the board are formal audit reports or preset agendas.

正解:A

質問 # 168

An organization decides to create an internal audit function and hires a new chief audit

executive (CAE). Which of the following should the CAE first consider when developing the internal audit process?

- A. Requirements of the external auditors to ensure an efficient coordination of audit effort.

- B. An appropriate training plan for audit staff.

- C. Sufficient resources to adequately meet the needs of the annual audit plan.

- D. Alignment of internal audit objectives with the organization's strategic plan.

正解:D

質問 # 169

Which of the following statements regarding the use of external contracted services by the chief audit executive (CAE) is false?

- A. The CAE's responsibility is not impaired by engaging an external expert.

- B. The expert should be directed by the objectives and scope of work.

- C. The external expert could have a prior relationship with the audit client.

- D. The audit report should not disclose the use of contracted services.

正解:D

質問 # 170

After completing a net present value (NPV) calculation on a proposed project, an analyst explores the change in NPV with changes in the interest rate. This additional analysis is referred to as:

- A. Decision analysis.

- B. Variance analysis.

- C. simul-ation.

- D. Sensitivity analysis.

正解:D

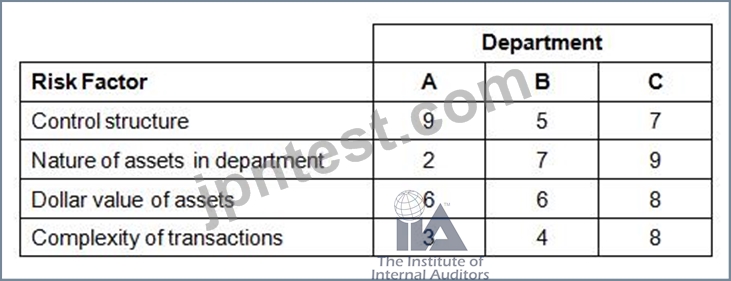

質問 # 171

A bank uses a risk analysis matrix to quantify the relative risk of auditable entities. The analysis involves rating auditable entities on risk factors using a scale of 1 to 10, with 10 representing the greatest risk. A partial list of risk factors and the ratings given to three of the bank's departments is provided below:

Which of the following statements regarding risk in the department is true?

- A. As compared to departments A and C, department B has a stronger control system to compensate for the greater complexity of the department's transactions and dollar value of its assets.

- B. The nature of department A's control structure may be justified by the nature of the department's assets and the complexity of its transactions.

- C. The internal audit activity should schedule audits of department B more often than audits of department C because of the relative control strength of department C as compared to department B.

- D. The relative ranking of the departments in order of their risk, from greatest to least risk, is: A; C; B.

正解:B

質問 # 172

Which of the following is a weakness that is inherent in the use of the test data method to test internal controls in a computer-based accounting system?

- A. Conditions that were not specifically considered by the auditor may go untested.

- B. The approach requires the creation of "dummy companies," possibly destroying or altering actual company data in the process.

- C. The auditor must test many transactions with the same condition in order to achieve assurance that the condition is being detected.

- D. Inclusion of atypical data in the test data may cause errors to be noted on the exception report.

正解:A

解説:

Section: Volume A

質問 # 173

......

2023年最新の問題Certified Internal合格目指してIIA-CIA-Part2リアル試験をマスターせよ!:https://www.jpntest.com/shiken/IIA-CIA-Part2-mondaishu