443 お客様のコメント

443 お客様のコメント

真のシミュレーション環境

多くのユーザーが最初に試験に参加しているので、上記の試験と試験時間の分布は確かな経験を欠いており、したがって試験場所で混乱しがちであるため、つかむ時間は結局試験を完全に終わらせなかった。 この現象の発生を避けるために、CPA Financial Accounting and Reporting試験問題は各試験シミュレーションテスト環境に対応する製品を持ち、ユーザーはプラットフォーム上の自分のアカウントにログオンし、同時に試験シミュレーションに参加したいものを選択します。FAR試験問題は自動的にユーザーが実際のテスト環境のシミュレーションテストシステムと同じように提示され、ソフトウェア内蔵のタイマー機能は体系的な達成するために、ユーザーが時間をかけてより良い制御を助けることができます。FARテストガイドを使って問題を横から解決するためにユーザーのスピードを向上させるためにも。

簡潔な内容

分析後のすべての種類の試験の暦年に基づくエキスパートによるFAR試験問題、それは開発動向に焦点を当てた試験論文に適合し、そしてあなたが直面するあらゆる種類の困難を要約し、ユーザーレビューを強調する 知識の内容を習得する必要があります。 そして他の教育プラットフォームとは異なり、CPA Financial Accounting and Reporting試験問題は暦年試験問題の主な内容が長い時間の形式でユーザーの前に表示されていないが、できるだけ簡潔で目立つテキストで概説されていますFARテストガイドは、今年の予測トレンドの命題を正確かつ正確に表現しており、トピックデザインのシミュレーションを通して細心の注意を払っています。

私たちのCPA Financial Accounting and Reporting研究問題は質が高いです。 それでテストの準備をするためのすべての効果的で中心的な習慣があります。 私たちの職業的能力により、FAR試験問題を編集するのに必要なテストポイントに同意することができます。 それはあなたの難しさを解決するための試験の中心を指しています。 最も重要なメッセージに対するFARテストガイドの質問と回答の最小数で、すべてのユーザーが簡単に効率的な学習を行えるようにし、余分な負担を増やさずに、最後にFAR試験問題にユーザーがすぐに試験合格できるようにします。

コースの簡単な紹介

ほとんどのユーザーにとって、関連する資格試験へのアクセスが最初であるかもしれないので、資格試験に関連するコース内容の多くは複雑で難解です。 これらの無知な初心者によれば、FAR試験問題は読みやすく、対応する例と同時に説明する一連の基本コースを設定し、CPA Financial Accounting and Reporting試験問題でユーザーが見つけることができるようにしました 実生活と学んだ知識の実際の利用に対応し、ユーザーと記憶の理解を深めました。 シンプルなテキストメッセージは、カラフルなストーリーや写真の美しさを上げるに値する、FARテストガイドを初心者のためのゼロの基準に合うようにし、リラックスした幸せな雰囲気の中でより役立つ知識を習得します。 団結の状態を達成するために。

AICPA CPA Financial Accounting and Reporting 認定 FAR 試験問題:

1. Which of the following should be disclosed in a summary of significant accounting policies?

I. Management's intention to maintain or vary the dividend payout ratio.

II. Criteria for determining which investments are treated as cash equivalents.

III. Composition of the sales order backlog by segment.

A) I and III.

B) I only.

C) II and III.

D) II only.

2. During a period when an enterprise is under the direction of a particular management, its financial

statements will directly provide information about:

A) Neither enterprise performance nor management performance.

B) Management performance but not directly provide information about enterprise performance.

C) Enterprise performance but not directly provide information about management performance.

D) Both enterprise performance and management performance.

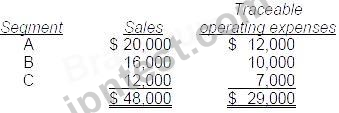

3. Taft Corp. discloses supplemental industry segment information. The following information is available for

1 992:

Additional 1992 expenses, not included above, are as follows:

Indirect operating expenses $7,200

General corporate expenses 4,800

Segment C's 1992 operating profit was:

A) $2,000

B) $3,200

C) $5,000

D) $2,600

4. Which of the following describes how comprehensive income should be reported?

A) May be reported in a combined statement of income and comprehensive income or disclosed within a

statement of stockholders' equity; separate statements of comprehensive income are not permitted.

B) May be reported in a separate statement, in a combined statement of income and comprehensive

income, or within a statement of stockholders' equity.

C) Should not be reported in the financial statements but should only be disclosed in the footnotes.

D) Must be reported in a separate statement, as part of a complete set of financial statements.

5. In Yew Co.'s 1992 annual report, Yew described its social awareness expenditures during the year as

follows:

"The Company contributed $250,000 in cash to youth and educational programs. The Company also gave

$ 140,000 to health and human-service organizations, of which $80,000 was contributed by employees

through payroll deductions. In addition, consistent with the Company's commitment to the environment,

the Company spent $100,000 to redesign product packaging."

What amount of the above should be included in Yew's income statement as charitable contributions

expense?

A) $490,000

B) $310,000

C) $410,000

D) $390,000

質問と回答:

| 質問 # 1 正解: D | 質問 # 2 正解: C | 質問 # 3 正解: C | 質問 # 4 正解: B | 質問 # 5 正解: B |